- 24 JAN 2017

Failure to Pass FATCA Could Mean Economic Hardship for You!

Your grocery bill, transportation costs, everyday banking transactions and the overall ease of doing business will be negatively impacted, if we fail to pass legislation to enforce the Foreign Account Tax Compliance Act (FATCA), when it returns to Parliament in February.

Your grocery bill, transportation costs, everyday banking transactions and the overall ease of doing business will be negatively impacted, if we fail to pass legislation to enforce the Foreign Account Tax Compliance Act (FATCA), when it returns to Parliament in February.

However once enacted, FATCA legislation, has little direct impact on Trinidad and Tobago citizens.

The law was designed to identify US persons living abroad or with assets and business interests outside of the US, for tax collection purposes.

Financial institutions worldwide have been asked to share information on their US clients with the US Inland Revenue Service (IRS).

In many cases this request cannot be granted without some adjustments to local law.

Here at home, we have introduced the Tax Information Exchange Agreements Bill, 2016 to facilitate FATCA.

There are, however, stiff penalties for any country that refuses to comply.

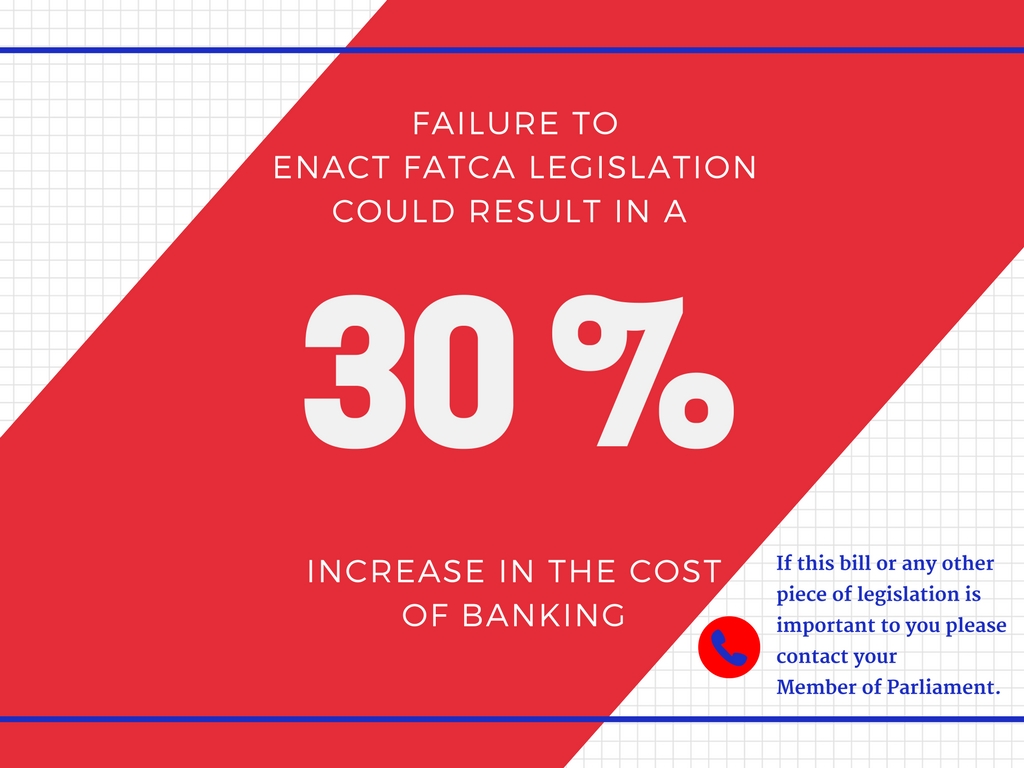

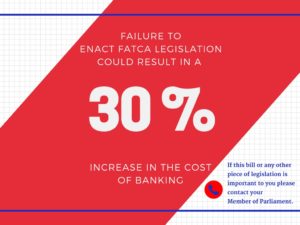

Under FATCA, US financial institutions must withhold 30 per cent of payments made to foreign financial institutions that do not agree to identify and report information on their US account holders.

The severity of this penalty becomes clearer when we examine how dependent our day-to-day transactions are on access to the US financial system.

Our ability to import food and raw materials for our manufacturing sector, make purchases with credit cards, do money transfers and buy online are all reliant on our banks maintaining a relationship with the US financial sector. Non-compliance means that the costs associated with these transactions will automatically increase by at least 30 per cent.

This will undoubtedly have an impact on our local economy and trigger new levels of inflation.

FATCA, along with Anti-Money Laundering and Counter Terrorism Financing laws, seek to bring more regulatory control to international banking practices.

Non-compliance will signal to the international community that we are not serious about combating corruption, white collar crime and tax evasion.

Increased scrutiny on financial fraud and new regulations to stem money laundering and terror finance have resulted in a practice called “de-risking” or “de-banking,” which occurs when banks pull out of certain lines of business, regions or individual countries.

Over the last four years, US financial institutions have ended their relationship with regional banks across the Caribbean as they remove potentially risky business from their books.

The Belize Government, for example, was accused by the US State Department of continuing to encourage off shore financial activities that are vulnerable to money laundering and terror financing.

Many of Belize’s banks have now found themselves cut off from US financial institutions. And it has had a deleterious effect on their economy.

The Government of Trinidad and Tobago understands the importance of safeguarding the banking sector and our international reputation.

In a few days, the fourth meeting of the Joint Select Committee, convened to consider and report on FATCA will begin. The Committee is mandated to consider and report on the Tax Information Exchange Agreements Bill 2016 by February 3, 2017.

When the bill returns to Parliament it will require a three fifths majority for passage.

If this bill or any other piece of legislation is important to you please contact your Member of Parliament.